Selling a business is one of the most important decisions an entrepreneur can make. Whether you’ve built your company from scratch, inherited it, or acquired it years ago, the time may come when you’re ready to move on. While many business owners dream of a quick, profitable exit, the reality is that selling a business can be slow, complex, and stressful. The good news? Taking the steps can significantly shorten the sales timeline and increase your chances of closing a deal at a fair price. This article breaks down exactly how to sell a business fast and provides tips to market your business for sale without sacrificing value, so you can transition smoothly to your next chapter.

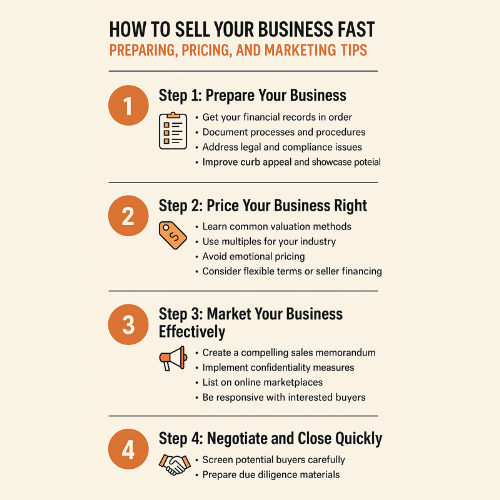

Step 1: Prepare Your Business for Sale

If you want to sell a business fast, preparation is key. Your business should be polished, organized, and ready for potential buyers to see its full value. Buyers aren’t just purchasing your current profits; they’re investing in future stability and growth. Preparation helps you showcase that potential and reduces any red flags that could slow down negotiations.

Get Your Financials in Order

Well-organized financial records are the foundation of a successful sale.

- Accurate records: Prepare up-to-date, reliable financial statements (profit and loss statements, balance sheets, tax returns for at least the last three years).

- Separate personal expenses: Remove non-business expenses that may have run through the company. This makes earnings more accurate and appealing.

- Demonstrate profitability: Highlight consistent revenue and strong margins. If profits recently dipped, be ready to explain why.

- Third-party review: Having an accountant prepare or audit your statements adds credibility and reassures buyers that the data is trustworthy.

Streamline Operations

A business that runs smoothly without the owner’s constant involvement is far more attractive.

- Document SOPs: Create standard operating procedures for major functions like sales, marketing, HR, and customer service.

- Train managers: Empower key staff to handle day-to-day responsibilities, reduce their dependency on you so the business doesn’t collapse without your presence.

- Cut inefficiencies: Eliminate redundant processes, renegotiate vendor contracts, or automate routine tasks to improve margins.

- Show scalability: Demonstrate that your systems can handle growth without needing major overhauls.

Address Legal and Compliance Issues

Unresolved legal or compliance matters can scare away buyers or delay closings. Clean up potential liabilities before listing.

- Contracts: Ensure customer contracts, leases, and supplier agreements are current and transferable.

- Licenses and permits: Verify that your business is operating with all required local, state, or federal approvals.

- Intellectual property: Protect trademarks, patents, copyrights, or proprietary processes to secure long-term value.

- Disputes: Resolve or disclose any ongoing lawsuits or tax issues upfront to avoid unpleasant surprises in due diligence.

Enhance “Curb Appeal”

First impressions count. When your business looks organized, profitable, and ready to thrive under new ownership, buyers are more likely to make offers quickly and with greater confidence.

- Physical improvements: Refresh signage, décor, or equipment if outdated.

- Digital presence: Update your website, polish social media profiles, and ensure branding is consistent.

- Customer testimonials: Gather reviews, success stories, or case studies that highlight your business’s reputation and market position.

- Growth potential: Point out expansion opportunities (new products, markets, or partnerships) so buyers can envision scaling.

Step 2: Price Your Business Right

Selling a business fast requires the right pricing. One of the most common reasons businesses sit on the market for months, or never sell at all, is unrealistic pricing. An inflated asking price discourages serious buyers, while undervaluing your business leaves money on the table. The goal is to find the sweet spot: a price that is fair, attractive, and grounded in market reality.

Understand Valuation Methods

There isn’t a single “correct” way to value a business; different industries and buyers emphasize different factors. Many sellers benefit from blending methods, rather than relying on one alone. Here are the three primary methods:

- Market Approach: Compares your business to recent sales of similar businesses. For instance, if cafés in your region are selling for 2.5x annual earnings, that benchmark helps set expectations.

- Income Approach: Looks at projected future earnings and discounts them to today’s value (discounted cash flow). This method is especially useful for businesses with stable or growing profits.

- Asset Approach: Adds up the value of tangible assets (equipment, real estate, inventory) and intangible assets (brand value, customer lists, IP) minus liabilities. It’s often used for asset-heavy industries like manufacturing or construction.

Use Multiples

Many buyers and brokers use earnings multiples as a quick gauge of value. These multiples vary by industry, risk level, and growth potential:

- Small service business: Often sells for 2–3x SDE (Seller’s Discretionary Earnings).

- Retail or restaurants: Typically 1.5–3x SDE depending on location and stability.

- Tech or SaaS companies: Can fetch 5–7x EBITDA or more if recurring revenue is strong.

Avoid Emotional Pricing

It’s natural for owners to feel their business is worth more because of years of effort, personal sacrifices, or sentimental value. However, buyers only care about future cash flow, stability, and growth potential. Overpricing due to emotion can turn away serious buyers, cause listings to sit stale, leading to price drops later, and damage your credibility. Detach emotionally and focus on objective metrics.

Offer Flexible Terms

Sometimes it’s not just about the price tag; it’s about how the deal is structured. Offering creative financing can make your business accessible to more buyers and help close faster:

- Seller Financing: You finance part of the purchase price and collect payments over time with interest. This reassures buyers and widens the buyer pool.

- Earn-Outs: Part of the price is contingent on the business hitting certain performance targets post-sale. This reduces risk for buyers and shows your confidence in the business’s future.

- Installment Plans: Spreading payments can make a larger purchase price manageable.

Step 3: Market Your Business Effectively

A well-prepared, properly priced business still won’t sell quickly without visibility. Correct marketing is necessary to sell a business fast. This is the stage where speed happens. The more qualified eyes you get on your business, the higher the chance of receiving serious offers. The goal is to craft a professional presentation, protect sensitive information, and get in front of the right buyers. Follow these tips to market your business for sale:

Create a Strong Sales Memorandum

Think of your sales memorandum (sometimes called an information memorandum or prospectus) as your business’s resume. It’s a polished document that presents the company in the best light and gives buyers the information they need to take the next step. A strong memorandum should include:

- Company overview: History, mission, and how the business operates.

- Products/services: Clear explanation of what you sell and how you serve customers.

- Financial highlights: Revenue, profit, growth trends, and key performance metrics.

- Customer base & market position: Who your clients are, retention rates, and competitive edge.

- Growth opportunities: Expansion possibilities, new markets, or product lines.

- Reason for sale: Buyers want to know why you’re exiting (retirement, new venture, etc.).

Protect Confidentiality

Selling fast doesn’t mean broadcasting sensitive details to the world. If employees, competitors, or customers learn too early, it can create unnecessary risk. Protecting confidentiality is essential:

- Blind ads: Post general descriptions of the business (industry, location, size) without revealing identity.

- NDAs (Non-Disclosure Agreements): Require serious buyers to sign before releasing detailed financials, contracts, or client lists.

- Controlled disclosures: Share information in stages, start with broad facts, then provide specifics only to vetted buyers.

Choose Your Channels

Another important tip to market your business for sale is choosing he right marketing channels. Where you list and promote your business has a direct impact on how quickly it sells. Consider a mix of strategies:

- Online listing platforms: Sites like WorldBusinessesForSale.com connect sellers with a global pool of motivated buyers. Listing here ensures wide exposure.

- Business brokers: Brokers often have buyer databases, industry knowledge, and negotiation experience that save time.

- Industry networks: Trade associations, LinkedIn groups, professional forums, and local chambers of commerce are excellent for targeting buyers in your sector.

- Direct outreach: In some cases, approaching competitors, suppliers, or even employees can lead to fast, mutually beneficial deals.

Optimize Your Listing

The goal is to spark enough interest for buyers to request more details quickly. Whether you’re working with a broker or posting online, your listing needs to stand out:

- Headline: Use a clear, compelling headline (“Profitable Local Café with Loyal Customer Base” instead of “Café for Sale”).

- Highlights: Showcase what makes your business unique (strong customer loyalty, recurring revenue, prime location).

- Visuals: Add professional photos of your space, equipment, or products; charts showing growth trends; and testimonials if available.

- Clarity: Avoid jargon. Write in a buyer-friendly way that emphasizes value.

Be Responsive

Another tip to market your business for sale is to be responsive. Once inquiries start coming in, the speed of response can make or break momentum:

- Reply to buyer questions promptly and professionally. Buyers often explore multiple opportunities at once. If you’re slow to respond, they may shift attention to a competitor.

- Provide the requested documents quickly to keep negotiations moving.

- Be flexible with call or meeting times; delays can lead to lost interest.

Marketing isn’t just about finding buyers. It’s about finding the right buyers quickly, presenting your business professionally, and keeping the process moving through responsiveness and confidentiality. When done well, marketing turns a prepared, fairly priced business into a fast, successful sale.

Step 4: Negotiate and Close Quickly

Even when a business is well-prepared, priced fairly, and you follow the above tips to market your business for sale, deals can stall in the final stages. Proper negotiation and closing techniques help you sell a business fast. These are often the most time-consuming parts of a sale, but with planning and the right mindset, you can accelerate this process and reach the finish line smoothly.

Pre-Screen Buyers

Not every inquiry will come from a qualified or serious buyer. Taking time to pre-screen saves you from wasted negotiations. This upfront filtering prevents delays and allows you to focus on serious prospects.

- Financial capacity: Ask for proof of funds or financing pre-approval early.

- Experience & motivation: Gauge whether the buyer has the background to run your business successfully.

- Timeline alignment: Ensure they’re looking to purchase soon, not “someday.”

Prepare Due Diligence Materials

Due diligence is where deals often slow down or fall apart. Having this material organized in a secure digital data room shows professionalism and keeps momentum going. Anticipate what buyers will request and have it ready:

- Financials: Tax returns, profit/loss statements, and payroll records.

- Contracts: Leases, vendor agreements, and client contracts.

- Employee information: Roles, responsibilities, and employment agreements.

- Operational manuals: SOPs, policies, and workflow documentation.

Stay Flexible

Speed often requires compromise. Being flexible on terms doesn’t mean giving away value; it means finding solutions that satisfy both parties.

- Payment structures: Consider installment payments, seller financing, or earn-outs.

- Transition support: Offer training or a handover period to reassure the buyer.

- Closing timeline: Adjust dates to meet the buyer’s financing or legal requirements.

Work With Professionals

Even experienced business owners benefit from expert guidance during closing. The right team ensures documents are correct, compliance is met, and disputes don’t derail progress. Though hiring professionals (an attorney, accountant, and maybe a broker) comes with costs, their involvement can save weeks of back-and-forth and protect you from costly mistakes.

Common Mistakes That Slow Down a Sale

- Overpricing: Deters buyers from even inquiring.

- Poor financials: Disorganized books kill confidence.

- Owner dependence: If the business can’t run without you, buyers hesitate.

- Hidden issues: Legal disputes or unspoken debts can derail deals.

- Slow response time: If you take days to reply, buyers lose interest.

If you’re ready to take action, consider listing your business on a reputable marketplace like World Businesses For Sale, where motivated buyers are actively searching right now. With the right foundation and exposure, your business could be someone else’s next big opportunity, and your successful exit could be just around the corner.

Conclusion

Selling your business fast is not a matter of luck. It’s about preparation, smart pricing, and following the right tips to market your business for sale. By streamlining your operations, establishing a fair value, and presenting your company to the right buyers, you can transform what might be a year-long process into a matter of months or even weeks.

To a Fitter Healthier You,

The Fitness Wellness Mentor

About the Author

Adriana Albritton holds a Master’s degree in Forensic Psychology, is certified in personal training, nutrition, and detoxification, and is the founder of FitnAll Coaching and its accompanying blog. She is the author of 28 Days to a New Life: A Holistic Program to Get Fit, Delay Aging, and Enhance Your Mindset, and a coauthor of The Better Business Book Volumes II and III. With a background in mental health, Adriana brings a holistic, science-backed approach to wellness. She combines mindset coaching, fitness, and nutrition to help people stay lean, energized, healthy, and centered. As part of Health Six FIT, she’s also helping reshape healthcare through AI-driven, integrative wellness education.